Infographic #3 - Financial Inclusion in Africa

Financial inclusion is on the rise across Africa.

In recent years, financial inclusion on the continent has primarily been driven by the rapid adoption of mobile money and electronic payment solutions. However, while strides have been made, access to credit remains challenging in many regions.

This infographic delves into the key financial inclusion metrics across Africa's prominent markets. When assessing financial inclusion, we consider three board parameters:

Access indicators: depth and reach of financial service e.g., number of POS devices in rural areas

Usage indicators: frequency and duration of a financial service over time e.g., number of transactions per bank account single opening

Quality indicators: alignment of financial products and services with the needs of clients e.g., range of options available.

Financial Inclusion Metrics across the Big 4 Markets in Africa

1. Nigeria

As of 2021, the Central Bank of Nigeria (CBN) reported that Nigeria's financial inclusion rate stood at 64% (1), with mobile money penetration at a noteworthy 16.9%. These numbers signify substantial progress in extending financial services to the population and can be attributed to several factors and developments including:

Regulatory reforms (2012 - 2014): CBN implemented regulatory reforms to promote financial inclusion. These reforms included the issuance of agency banking guidelines, which allowed banks to partner with agents (e.g., small shops and businesses) to provide banking services in underserved areas. This move helped bring banking services closer to people in rural and remote regions.

Biometric verification (2014): The launch of the Bank Verification Number (BVN) system in 2014 was a landmark development. It required all bank customers to undergo biometric verification, making it easier to identify and track customers across different banks. This initiative enhanced the credibility of the financial sector and increased confidence in formal banking systems.

2. Egypt

As of 2021, the Central Bank of Egypt (CBE) reported that Egypt’s financial inclusion rate stood at 56% (2), highlighting a significant shift toward formal banking services. This can be primarily attributed to the following reasons:

Banking sector reforms (2016 - 2019): Egypt's government and regulatory authorities undertook several reforms aimed at modernizing the banking sector. These reforms included efforts to encourage financial institutions to expand their services and reach underserved areas and populations, and to streamline banking procedures to improve the overall customer experience.

National ID registration (2009): The government's efforts to encourage citizens to register for national identification cards were pivotal (3). Having a valid national ID became a prerequisite for opening a bank account. This initiative helped formalize the financial sector and expand access to banking services to a broader segment of the population.

Government integration (2020): The government used bank accounts to distribute various subsidies and benefits, such as fuel subsidies and social welfare payments. This incentivized many Egyptians to open bank accounts to access these benefits, further driving financial inclusion (4).

3. South Africa

South Africa’s financial inclusion landscape is distinctive in its own right. As of 2021, the South African Reserve Bank (SARB) reported that South Africa’s financial inclusion rate stood at 80% (5), reflecting a relatively high level of financial inclusion compared to other African countries. This can be attributed to some of the following policies:

Introduction of the National Credit Act (2007): The National Credit Act significantly contributed to financial inclusion by regulating credit providers and making credit more accessible to a broader population while protecting consumers from predatory lending practices.

Government financial inclusion programs (2004 - 2009): The South African government introduced various programs aimed at expanding financial inclusion during this period. Initiatives like the Mzansi bank account and partnerships with community organizations helped individuals in marginalized areas open bank accounts and access essential financial services.

The country has a well-established banking sector, with a robust network of bank branches and ATMs, making financial services widely accessible to urban and rural populations.

South Africa has also seen significant growth in digital payments and fintech innovation, with mobile banking apps and contactless payments constituting more than 50% of payments and up to 60% of surveyed South Africans reported they’re likely to tap a smartphone to pay or make payment via digital wallets (6).

4. Kenya

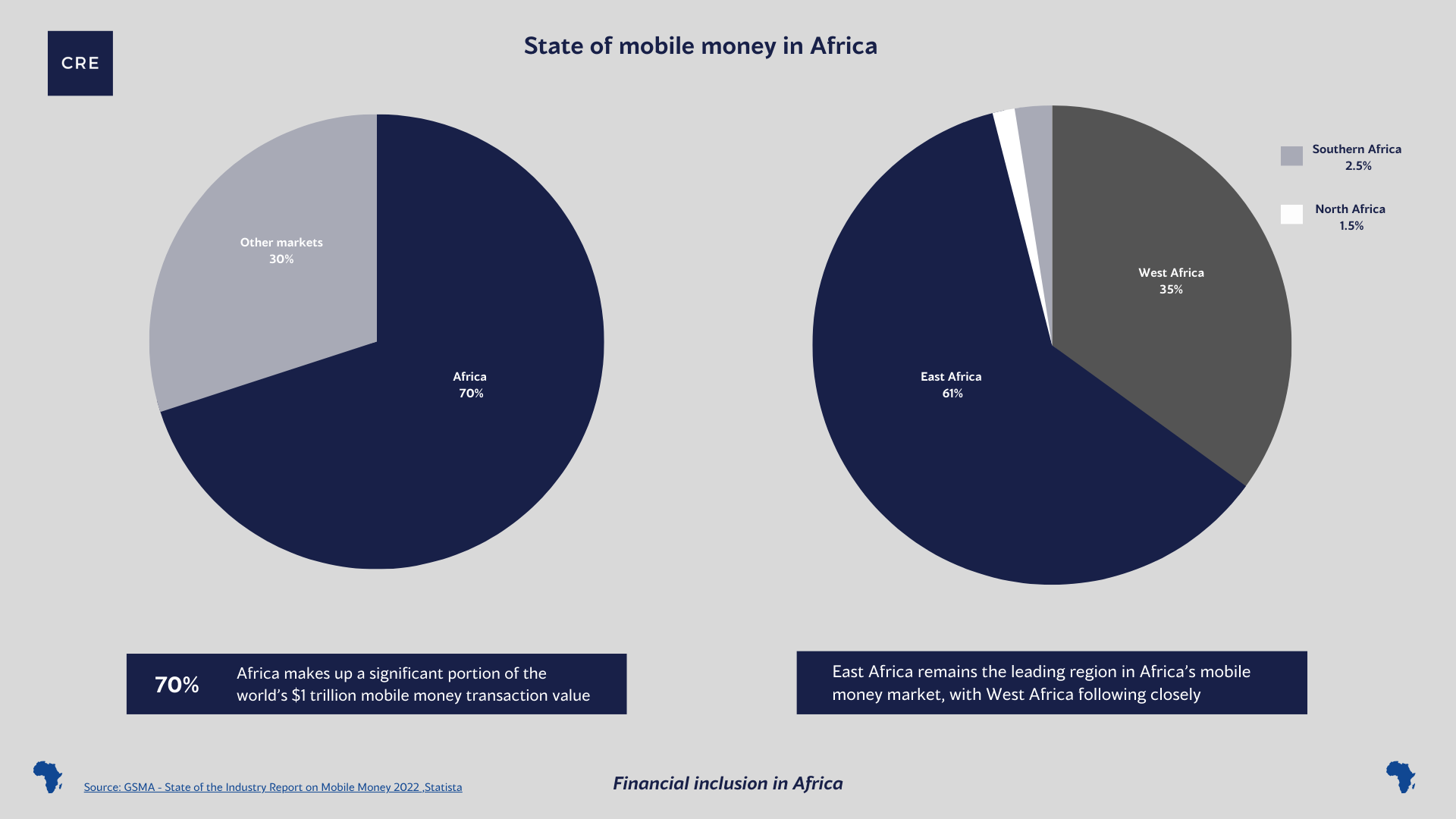

As of 2021, the Central Bank of Kenya (CBK) reported that Kenya's financial inclusion rate stood at 84% (7), with mobile money penetration at a staggering 73% (8). East Africa recorded over 50% of Africa's mobile money transaction value put at $832 billion in 2022, with Kenya as the market leader (9).

M-PESA revolution (2007): M-PESA, a mobile money network launched by Safaricom in 2007, revolutionized financial services in Kenya. It allows users to send and receive money, pay bills, and access microloans via mobile phones. The service quickly gained popularity due to its simplicity and accessibility, and remains a juggernaut with $19b+ in transaction volume as of 2022 (10).

Kenya's Digital Economy Blueprint (2019): The Kenyan government launched "Kenya's Digital Economy Blueprint” in 2019. This comprehensive policy framework aimed to harness digital technologies for economic development and financial inclusion. It included strategies to improve access to digital financial services, foster entrepreneurship, and enhance digital literacy, all of which contributed to a more inclusive financial landscape.

The rise of electronic payments

Electronic payment methods, including debit cards and digital wallets, are reshaping the landscape of financial services, making them more accessible and convenient for individuals and businesses alike.

In 2020, Africa's e-payment industry generated around $15 billion, with projections to reach approximately $40 billion by 2025 (11). This growth is attributed to the increasing adoption of digital payment methods. Notably, in Kenya, the percentage of the population over 15 years making or receiving digital payments surged from 2% in 2011 to 78% in 2021. In Egypt, it rose from 1% to 20% during the same period. In Nigeria and South Africa, similar increases were seen, with percentages going from 1% to 34% and 5% to 81%, respectively.

Access to credit: a continuing challenge

Despite progress within various financial products, credit accessibility remains a hurdle for many individuals and businesses. As of 2021, the average credit card penetration across 28 African countries remained at a modest 3.92% (12). Limited credit card access in Africa is attributed to factors including low income levels and a lack of credit history:

Low-income levels: Much of the African population has low to moderate income, which doesn't align with the income expectations for traditional credit card holders.

Lack of credit history: African individuals often lack established credit histories, making it difficult to qualify for credit cards.

Significant differences in credit card adoption are noticeable between Mauritius, with a penetration rate of 20.06%, and Tanzania, with just 0.31%. Mauritius' higher income levels drive greater credit card usage, while Tanzania's low penetration may be largely due to challenges in its financial infrastructure, common among African nations.

The road ahead

Comprehensive financial inclusion necessitates collaboration among governments, financial institutions, investors, and technology companies. Within our fintech portfolio, companies like Flutterwave, which specialises in payments and facilitating cross-border transactions, Stitch, which offers A2A payments, starting with electronic funds transfers, and Yoco, which offers Point of Sale (POS) solutions to small businesses, are aiming to help deepen financial inclusion on the African continent in various ways.

Sources

(1) The Central Bank of Nigeria:

https://www.cbn.gov.ng/DFD/Financialinclusion.asp

(2) The Alliance for Financial Inclusion:

https://www.afi-global.org/wp-content/uploads/2023/09/AFI_Maya-Annual-Report_2023.pdf

(3) Human Rights Watch:

https://www.hrw.org/reports/2007/egypt1107/3.htm

(4) The Central Bank of Egypt:

(5) Deloitte:

(6) Mastercard:

https://stitch.money/blog/an-overview-of-the-payments-ecosystem-in-south-africa

(7) Financial Sector Deepening Kenya (FSD):

(8) The World Bank:

https://elibrary.worldbank.org/doi/abs/10.1596/1813-9450-5988

(9) GSM Association:

https://www.gsma.com/sotir/wp-content/uploads/2022/03/GSMA_State_of_the_Industry_2022_English.pdf

(10) Statista:

(11) McKinsey:

(12) The Global Economy:

https://www.theglobaleconomy.com/rankings/people_with_credit_cards/Africa/